Money wins. The Hyperliquid stablecoin war ends where it started

Hyperliquid tried to move beyond USDC with USDH, but the final deal looks more like a renegotiation than a retreat.

Hyperliquid, the largest decentralized crypto exchange for perpetual futures by trading volume, spent months trying to answer a simple but uncomfortable question. Why does billions worth of stablecoin liquidity have to exist on their platform when they reap none of its benefits?

That question turned into the USDH contest in September 2025. Hyperliquid offered a validator-driven competition for the best team capable of issuing a native stablecoin, and Native Markets came out as the winner on September 14, beating off stronger contenders such as Paxos, BitGo, Ethena, and Frax.

Now the answer looks less like independence and more like renegotiation.

Coinbase said in a May 14 blog post that it will become the official treasury deployer of Circle's USDC stablecoin on Hyperliquid as an Aligned Quote Asset, or AQA, putting USDC into the role USDH was built to chase.

- Coinbase will manage the treasury-deployer role and share most reserve-yield revenue with the protocol.

- Circle, the issuer of USDC, will handle the technical deployment.

- Native Markets, the team behind USDH, has agreed to terms giving Coinbase the right to buy the USDH brand assets.

The companies have announced that USDH markets continue to work, and users will be able to trade USDH tokens for USDC or fiat currency without any additional costs.

But USDH will gradually sunset, while USDC will return to the center stage on Hyperliquid.

What's under the hood

Hyperliquid isn't abandoning the idea that stablecoin economics should benefit the protocol. But it does sound like it's abandoning the idea that a separate stablecoin has to be the main way to get there.

The whole stablecoin drama on Hyperliquid started because USDC already dominated the network, but the reserve yield on that stablecoin mostly belonged to Circle and Coinbase, not to Hyperliquid.

- Across, a bridge that integrated USDH, wrote in a blog post that about 95% of Hyperliquid's stablecoin deposits, or roughly $5.6 billion, were in USDC when the USDH proposal went to a validator vote.

- It also estimated that the reserve yield not flowing to Hyperliquid was worth about $150 million to $220 million a year, adding that USDH markets offered 20% lower taker fees, 50% higher maker rebates and 20% volume contribution amplification toward fee tiers.

In other words, USDH acted as a bargaining chip with a product wrapped around it.

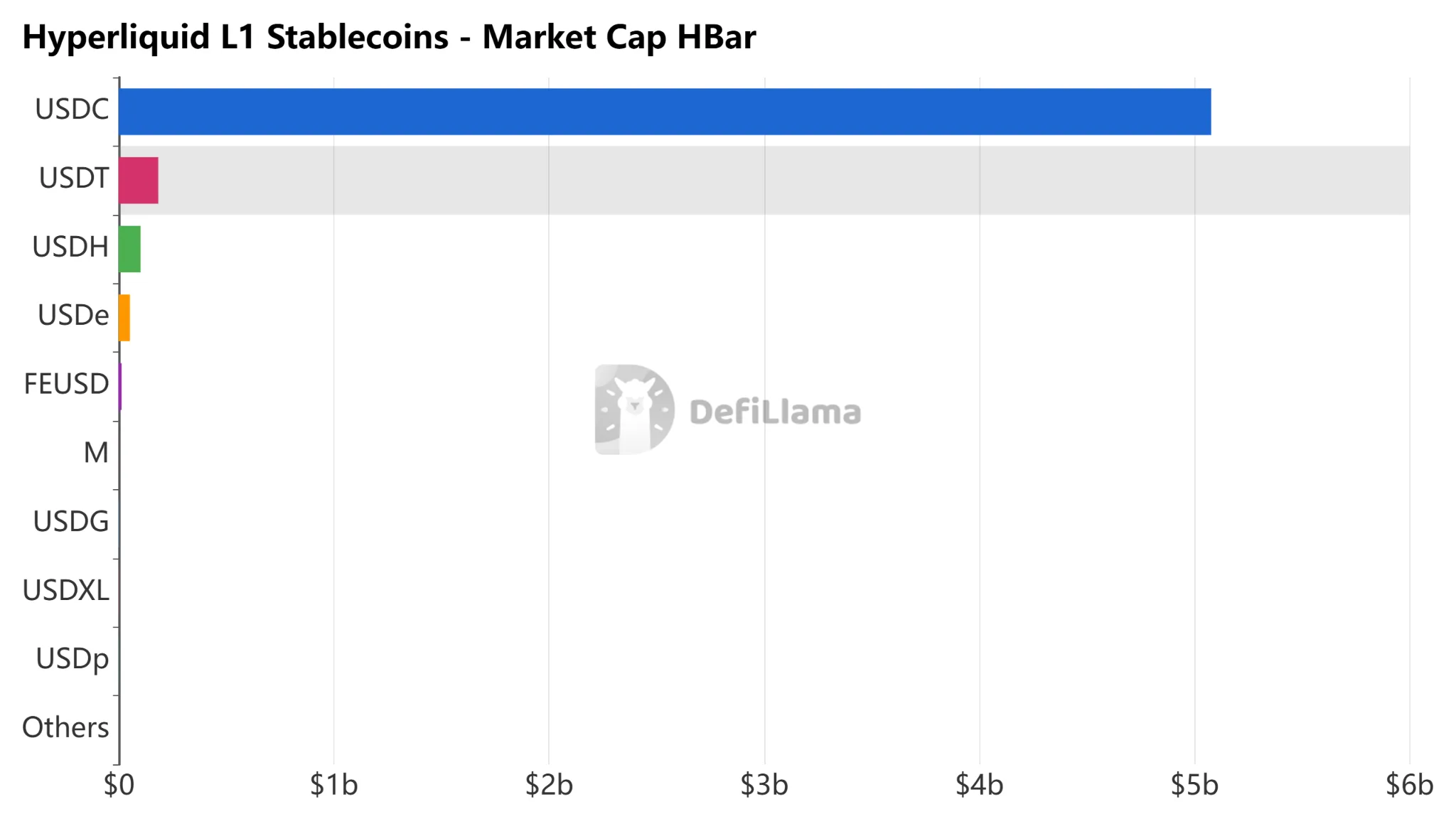

Hyperliquid stablecoins by their market capitalization on the network. Source: DefiLlama

However, there were some things that the market itself disagreed on. For example, DeFiLlama data shows USDC has $5 billion on the Hyperliquid blockchain and roughly $101.7 million of USDH, which makes USDC about 50 times larger than USDH on the network.

USDH lost the ticker war

Although USDH didn't become Hyperliquid's preferred stablecoin over USDC, it seems like it managed to alter the economics surrounding USDC on the platform.

Before USDH, USDC was the default rail and the yield economics largely sat outside Hyperliquid. After USDH, Coinbase is agreeing to make USDC more aligned with Hyperliquid's own economics.

So while the native stablecoin experiment didn't beat USDC in liquidity, it appears to have forced USDC to come back on better terms.

The scale of Hyperliquid made the USDH push harder from the start. DeFiLlama shows Hyperliquid with about $176.4 billion in 30-day perpetual volume, $8.89 billion in open interest and $627.2 million in annualized revenue.

Hyperliquid said Coinbase will share the "vast majority" of reserve-yield revenue with the protocol, but it hasn't published a clear formula showing the exact split, timing or duration of that arrangement.

- For context, Native Markets proposed that 50% of USDH reserve yield would go to the Hyperliquid Assistance Fund, which buys HYPE, while the other 50% would go toward USDH growth with builders, HIP-3 markets and HyperEVM apps.

- The team also said the point was to bring back to Hyperliquid the yield that Coinbase earned from USDC sitting on the network.

- Under Hyperliquid's updated aligned quote asset framework, stablecoin deployers share about 90% of cost-adjusted reserve-yield revenue from their Hyperliquid supply with the protocol. The treasury deployer also has to stake 500,000 HYPE, while the technical deployer has to stake another 500,000 HYPE.

- If Across' earlier estimate is used only as a loose proxy, 90% of that $150 million to $220 million range would imply about $135 million to $198 million a year potentially flowing back to the protocol.

- Using the lower current USDC supply figure of about $5 billion, the rough range would be closer to about $121 million to $177 million a year, before any differences in actual rate calculations.

The problem was easiest to see with HIP-4, Hyperliquid's outcome-market system. Those markets launched with USDH as collateral, so users who mostly held USDC had to switch into USDH before they could trade.

Now the opposite has been set to happen. According to Hyperliquid, canonical HIP-4 markets will be set up in a future network upgrade with USDC as the quote asset.

The remaining open question is how much of that money actually shows up. Hyperliquid says Coinbase will share the vast majority of reserve-yield revenue with the protocol, and AQAv2 points to about 90% of cost-adjusted reserve yield.

But the final dollar amount will depend on USDC supply, reserve rates, costs, validator-reported calculations and how long the arrangement lasts.

Hyperliquid tried to move beyond USDC with USDH, but the final deal looks more like a renegotiation than a retreat.